If a european licensing deal for an ALS drug commands €500M, one must wonder how much more NeuroSense’s seemingly superior ALS therapy could actually be worth? (NASDAQ: NRSN)*

In a revealing industry development, Prilenia Therapeutics just secured a €500 million ($540 million) European licensing deal for pridopidine with Ferrer – despite the fact that the drug didn’t meet it’s primary endpoints in clinical trials. This surprising valuation offers a rare glimpse into what NeuroSense Therapeutics’ (NASDAQ: NRSN)* pending partnership for its successful ALS drug PrimeC could be worth – suggesting a potential valuation multiple times higher than the company’s current $25 million market cap.

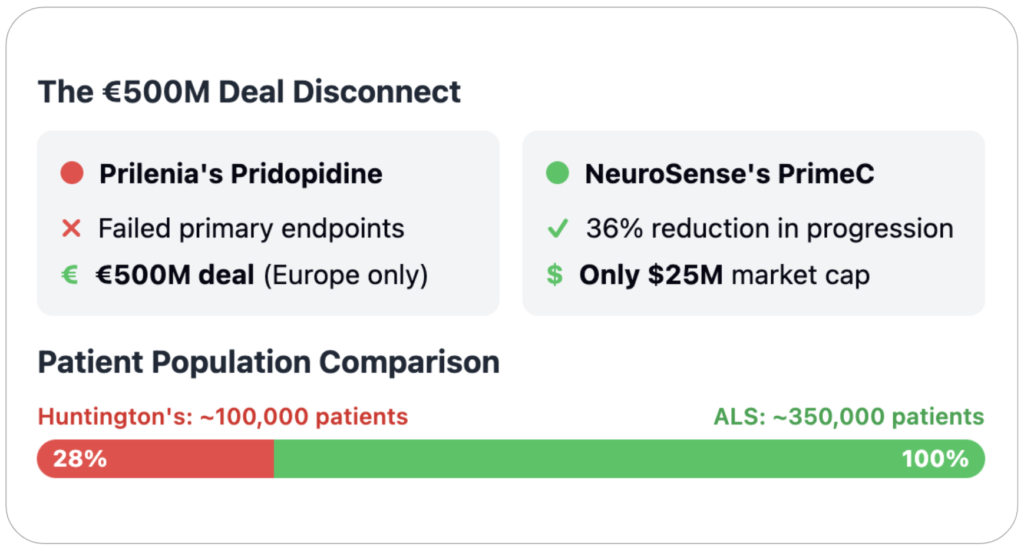

The Value Revelation: If Prlenia’s Drug Is Worth €500M, NeuroSense’s Deal Could Be Astronomical

The April 28 Prilenia-Ferrer agreement provides a critical benchmark for assessing NeuroSense’s pending partnership. Consider the stark contrast:

Prilenia’s pridopidine did not meet primary endpoints in both Huntington’s disease and ALS trials, only showing benefits in post-hoc subgroup analyses. Yet it commanded a €500M deal covering European rights only, with €125M ($135M) in upfront and near-term payments.

Meanwhile, NeuroSense’s PrimeC demonstrated statistically significant 36% reduction in ALS progression (p=0.009), showed 43% improvement in survival rates vs placebo, and achieved 58% better survival at 18 months (p=0.007). The company has a binding term sheet with a “leading global pharmaceutical company” potentially involving major territories.

This stark efficacy difference alone suggests NeuroSense’s deal could dwarf Prilenia’s €500M valuation. Yet NRSN’s entire market cap currently sits at just $25 million – creating a potential once-in-a-decade valuation disconnect.

Significantly Larger Market Potential

The numbers paint a clear picture of PrimeC’s superior market opportunity. ALS affects 350,000 people globally versus just 100,000 for Huntington’s disease. The ALS market is projected to reach $1-1.2 billion by 2030 according to Mordor Intelligence. Furthermore, pridopidine’s ALS program still requires a pivotal Phase 3 trial, while PrimeC has already shown statistically significant efficacy.

If European-only rights to a far more premature drug command €500M, what might global rights to a clinically successful ALS therapy be worth? The mathematics of comparable valuations suggests PrimeC’s partnership could easily reach into the billions.

NeuroSense’s Binding Term Sheet: The Countdown to Value Creation

While Prilenia’s deal is limited to Europe, NeuroSense’s December 2024 announcement revealed a binding term sheet with a global pharmaceutical company that could involve far more valuable territories. Though initially expected to close in Q1 2025, CEO Alon Ben-Noon recently confirmed discussions remain “active and constructive,” with the delay attributed to “the complexity of this multi-regional partnership.”

With Prilenia’s deal now establishing concrete valuation metrics for neurodegenerative disease treatments, NeuroSense’s ongoing negotiations have an established industry reference point that strongly supports a substantial premium valuation.

The Most Compelling Risk-Reward in Biotech Today?

At its current ~$25 million market cap, NeuroSense represents what some might call the most asymmetric risk-reward profile in the biotech sector. The company has a binding term sheet already in place, superior clinical data versus Prilenia’s pridopidine, a larger addressable market, and multiple near-term catalysts including Phase 3 initiation (mid-2025) and potential Canadian commercialization (H1 2026).

The Prilenia-Ferrer deal doesn’t just provide a comparison – it effectively establishes a floor for what NeuroSense’s partnership should be worth, suggesting the potential for returns many multiples higher than the company’s current valuation.

The Verdict: Potentially Massively Undervalued Based on Established Industry Metrics

With Alliance Global Partners maintaining a $7.50 price target (500%+ premium to current levels), Some members of Wall Street seem to have already recognized NeuroSense’s potential. But the Prilenia deal provides strong evidence that even this target could be conservative once a definitive agreement is announced.

The stark reality is clear: if a drug that didn’t meet its primary endpoints can secure a €500M deal for European rights alone, a therapy with statistically significant efficacy in a larger market could command a substantially higher valuation across broader territories.

For investors, the clock is ticking on what might turn out to be one of the most compelling value disconnects in the biotechnology sector today – a disconnect that the Prilenia-Ferrer deal has now quantified in precise financial terms.

Read more Articles from The Finance Herald

- Balancing National Security and Civil Liberties: U.S. Intelligence Insights on Vaccine Mandate Opposition

- FBI’s Renewed Focus: High-Profile Investigations Under Scrutiny Amid Calls for Public Engagement

- The Great Financial Shift: Navigating the New Global Economic Paradigm

- Navigating the Stealth Bear Market: A Strategic Approach to Risk Management and Opportunity

- Tensions Rise as Trump Critiques Putin Amid Escalating Ukraine Conflict

Subscribe for More Reports

* Legal Disclaimer & Disclosure: Nothing in this report constitutes financial or investment advice, nor does it represent an offer to buy or sell securities. This report is published by Wall Street Wire™ . The operators of Wall Street Wire, arx advisory, are not registered brokers, dealers, or investment advisers. This report contains and is a form of paid promotional content or advertisement for NeuroSense Therapeutics and was produced as part of their paid subscription to Wall Street Wire. This report has not been reviewed or approved by NeuroSense Therapeutics prior to publication. The operators of wall street wire have received or are expected to receive a monthly recurring fee of five thousand united states dollars via wire transfer from NeuroSense Therapeutics as part of an ongoing agreement starting March 17, 2025 in return for social media distribution and promotional coverage services, and receive additional compensation for non promotional unrelated data and advisory services on top of that. They do not hold any shares in NeuroSense Therapeutics. Please review the full disclaimers and compensation disclosures here for further details: redditwire.com/terms. We are not responsible for the price targets mentioned in this article nor do we endorse them, they are quoted based on publicly available news reports believed to be reliable and additional or price targets may exist that may not have been quoted. Readers are advised to refer to the full reports mentioned on various systems and the disclaimers/disclosures they may be subject to. As of the time of this report, the authors hold no shares in any of the companies mentioned.